According to a recent survey, more and more Americans are concerned about a possible recession. Those concerns were validated when the Federal Reserve met and confirmed they were strongly committed to bringing down inflation. And, in order to do so, they’d use their tools and influence to slow down the economy.

All of this brings up many fears and questions around how it might affect our lives, our jobs, and business overall. And one concern many Americans have is: how will this affect the housing market? We know how economic slowdowns have impacted home prices in the past, but how could this next slowdown affect real estate and the cost of financing a home?

According to Mortgage Specialists:

“Throughout history, during a recessionary period, interest rates go up at the beginning of the recession. But in order to come out of a recession, interest rates are lowered to stimulate the economy moving forward.”

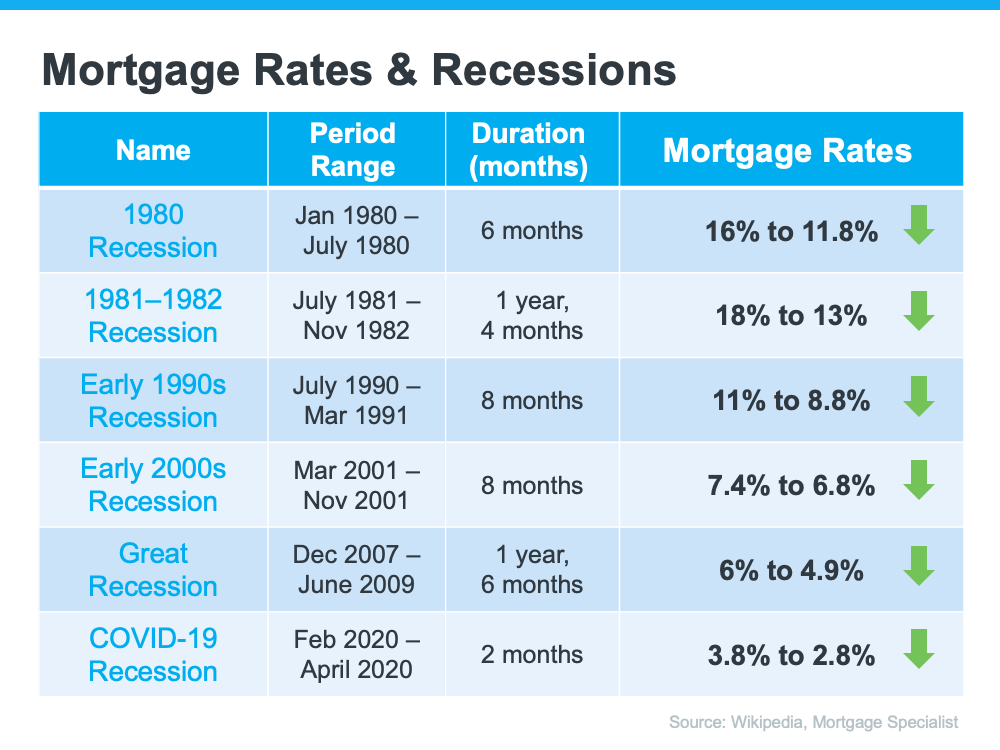

Here’s the data to back that up. If you look back at each recession going all the way to the early 1980s, here’s what happened to mortgage rates during those times (see chart below):

As the chart shows, historically, each time the economy slowed down, mortgage rates decreased. Fortune.com helps explain the trend like this:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

And while history doesn’t always repeat itself, we can learn from it. While an economic slowdown needs to happen to help taper inflation, it hasn’t always been a bad thing for the housing market. Typically, it has meant that the cost to finance a home has gone down, and that’s a good thing.

Bottom Line

Concerns of a recession are rising. As the economy slows down, history tells us this would likely mean lower mortgage rates for those looking to refinance or buy a home. While no one knows exactly what the future holds, you can make the right decision for you by working with a trusted real estate professional to get expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Chrysti Tovani is a Fair Oaks Real Estate Advisor, Transition Specialist, and the author of Downsizing with Intention. She helps homeowners sell long held homes, downsize with clarity, and navigate major life transitions with confidence and strategic guidance.

With decades of experience in real estate, mortgage, and title, Chrysti brings deep industry knowledge and thoughtful preparation to every transaction. Her approach blends strategic home marketing, skilled negotiation, and emotional intelligence, ensuring that each move is handled with both precision and care.

As the founder of I Love Fair Oaks, a hyperlocal media platform highlighting trusted businesses and community life in Fair Oaks, California, Chrysti has built an integrated authority ecosystem that connects real estate expertise with community leadership.

Her work centers on clarity, visibility, and long term legacy, helping clients move forward with confidence while strengthening the community she serves.

When you think of homeownership, what’s the first thing that comes to mind? Chances are you might focus on the non-financial benefits, like the security or stability a home provides. But what about equity? While it can be overlooked, a homeowner’s equity helps build long-term wealth over time. Here’s a look at what equity is […]

When you think of homeownership, what’s the first thing that comes to mind? Chances are you might focus on the non-financial benefits, like the security or stability a home provides. But what about equity? While it can be overlooked, a homeowner’s equity helps build long-term wealth over time. Here’s a look at what equity is […]

A recent survey from Bankrate asks prospective buyers to identify the biggest obstacles in their homebuying journey. It found that 36% of those polled said saving for a down payment is one of their primary hurdles to buying a home. If you feel the same way, the good news is there are many down payment […]

A recent survey from Bankrate asks prospective buyers to identify the biggest obstacles in their homebuying journey. It found that 36% of those polled said saving for a down payment is one of their primary hurdles to buying a home. If you feel the same way, the good news is there are many down payment […]

![Have You Thought About Why You Might Want To Sell Your House? [INFOGRAPHIC]](https://chrystitovani.com/wp-content/uploads/2023/03/Have-You-Thought-About-Why-You-Might-Want-To-Sell-Your-House-KCM-Share.png)

![Have You Thought About Why You Might Want To Sell Your House? [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230323/Have-You-Thought-About-Why-You-Might-Want-To-Sell-Your-House-KCM-Share.png)

Many people are reaching the point in their lives when they need to decide where they want to live when they retire. If you’re a homeowner approaching this stage, you have several options to explore. Jessica Lautz, Deputy Chief Economist and Vice President of Research at the National Association of Realtors (NAR),

Many people are reaching the point in their lives when they need to decide where they want to live when they retire. If you’re a homeowner approaching this stage, you have several options to explore. Jessica Lautz, Deputy Chief Economist and Vice President of Research at the National Association of Realtors (NAR),